The ongoing geopolitical tensions in the Middle East, primarily involving Iran, Israel, and the United States, have sent a significant shockwave through the global energy market. This disruption is not merely political in nature; it is deeply structural, driven by the concentration of critical energy infrastructure and key exporting actors in the region.

One of the most strategic choke points globally is the Strait of Hormuz, through which approximately 20% of global oil and liquefied natural gas (LNG) exports transit. This makes it arguably the most critical energy gateway in the world today.

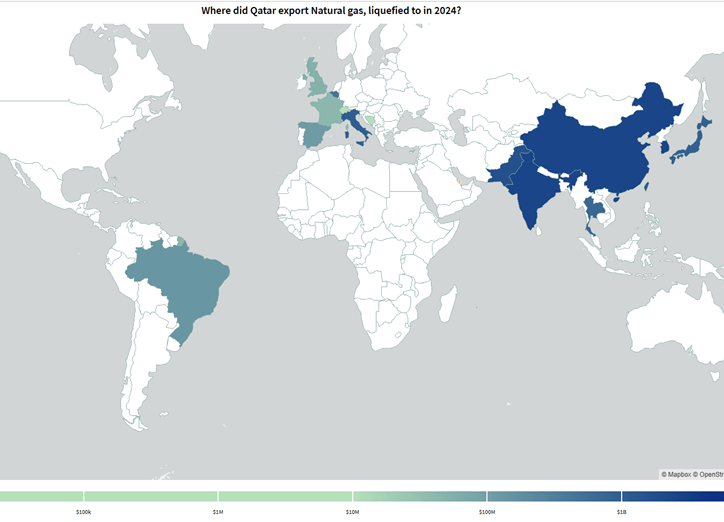

The region’s importance is further amplified by the presence of major exporters. Qatar stands as the world’s second-largest LNG exporter after the United States, with its production heavily reliant on uninterrupted maritime access through Hormuz.

The United Arab Emirates and Iran also play a significant role as oil exporters. However, international sanctions have forced Iranian exports to be sold at discounted prices, compensating importers for elevated geopolitical and legal risks. A key asset in this ecosystem is Kharg Island, which accounts for over 80% of Iran’s oil exports.

The combination of concentrated supply, critical infrastructure, and geopolitical instability among key players, creates a fragile equilibrium. Any disruption, particularly in Hormuz, has immediate and far-reaching consequences for global energy flows.

Given the present magnitude of the geopolitical tensions and the strategic importance of the region, one would expect oil prices to surge dramatically. However, Brent (a global pricing benchmark) crude is currently trading at approximately $107 per barrel, well below what the situation would typically justify.

This apparent disconnect suggests that current prices do not fully reflect the underlying supply shock, at least not yet. Specifically, they fail for the moment to capture the disruption of oil transit through the Strait of Hormuz caused by Iranian intervention.

One reason for this could be that oil prices might currently be shaped more by the speculative nature of financial markets. Oil is one of the most heavily traded commodities globally, and pricing could be more influenced by trader sentiment rather than purely physical supply-demand dynamics.

Market participants may be reacting optimistically to high-level political signals, particularly statements from US President Donald Trump regarding potential protection of oil flows, a swift resolution in Iran, or the prospect of a ceasefire that would reopen Hormuz. These political narratives, especially when coming from powerful and directly involved leaders, could sometimes carry more immediate weight in pricing than actual supply disruptions.

Additionally, the oil market was already oversupplied prior to the conflict. This created a substantial buffer that is currently absorbing the shock. However, the critical question remains: how long can this buffer hold?

Another key factor is timing. Many oil tankers had already exited Hormuz before the escalation and subsequent disruption. As a result, demand-side markets have not yet fully absorbed existing shipments. Once they do, the mismatch between stable or rising demand and a sudden contraction in supply will become evident.

When physical market realities catch up with financial market expectations, a sharp price correction is likely. Under such conditions, oil prices could escalate rapidly, potentially reaching $200 per barrel.

At present, the situation can be described as a moderate escalation scenario, not in terms of energy disruption, which is already significant, but in terms of military responses among the major actors involved.

Following Israeli strikes on the South Pars natural gas field, Iran responded forcefully yet with a degree of strategic restraint. Its retaliation resulted in damage to approximately one-fifth of Qatar’s Ras Laffan LNG facilities, a critical hub for global gas exports.

Saudi Arabia holds a strategic advantage through its East-West pipeline system, known as Petroline, which allows oil to bypass Hormuz by transporting it from the Persian Gulf to the Red Sea. This infrastructure acts as a partial mitigation mechanism against disruptions in the Strait.

In a similar strategic approach to Saudi Arabia, the United Arab Emirates has developed a backup solution to bypass the Strait of Hormuz through the Habshan-Fujairah Pipeline, commonly referred to as the Habshan Pipeline. This infrastructure connects inland oil fields in Abu Dhabi to the port of Fujairah on the Gulf of Oman, allowing crude exports to continue even in the event of disruptions in Hormuz. However, despite its critical role in enhancing supply security, the pipeline’s capacity, of up to approximately 2 million barrels per day, remains significantly lower than that of Saudi Arabia’s Petroline.

However, in the event of a major escalation, such as a joint U.S.-Israeli operation targeting Kharg Island, Iranian retaliation could intensify both in frequency and magnitude. Potential targets may include both Saudi Petroline and Emirati Habshan pipelines, and further attacks on Qatar’s Ras Laffan facilities.

Such developments would significantly amplify the supply shock beyond current levels. In this scenario, even the previously discussed $200 per barrel threshold may prove conservative, quickly becoming an outdated benchmark rather than a peak scenario.

A quantitative perspective highlights the scale of potential disruption:

These figures are aimed to illustrate a potential structural imbalance emerging in global supply chains, especially if the conflict escalates further and Iran targets Saudi and Emirati infrastructure.

Reference Note:

This analysis draws on insights from a Foreign Policy interview with Jason Bordoff, Director of the Center on Global Energy Policy at Columbia University, who highlights the disconnect between current oil prices and the scale of ongoing supply disruptions. Full original interview: https://foreignpolicy.com/2026/03/26/jason-bordoff-iran-war-energy-prices/