The Energy Market’s New Hot Spot

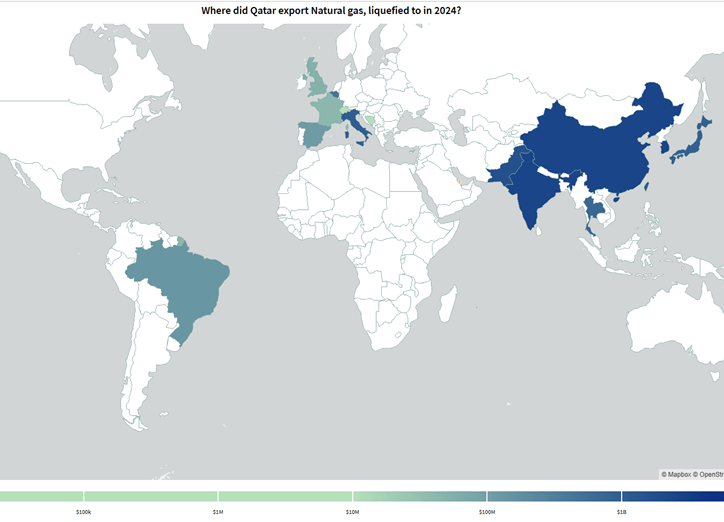

The escalating confrontation between Iran and the United States and Israel has rapidly transformed the Middle East into the central fault line of global energy markets. The current shock is likely to be more severe in LNG (liquified natural gas) markets than in oil markets. Unlike oil, whether crude or refined, natural gas trade is far more geographically concentrated, with a big share of global exports originating in the Persian Gulf. Qatar is the world's second largest LNG exporter after the US and the small emirate alone accounted in 2024 for approximately 15% of global LNG exports according to Harvard Atlas of Economic Complexity, amplifying the systemic impact of any disruption affecting its production or export capacity. At the centre of this disruption lies the Strait of Hormuz, through which approximately 20% of global LNG exports transit. The strait is geographically shared between Iran and Oman, but only Iran possesses the asymmetric capabilities required to effectively disrupt maritime traffic. Roughly 90% of these LNG flows (overly coming from Qatar and the United Arab Emirates) are directed toward Asia, particularly China, Japan, and South Korea, while economies such as India, Pakistan, and Bangladesh are also heavily exposed to disruptions in energy trade.

Recent hostilities, including Israeli strikes on Iranian gas infrastructure and subsequent Iranian retaliation targeting gas-related facilities connected to Qatar, have disrupted production capacity and introduced a level of uncertainty that energy markets are ill-equipped to absorb. Qatar has already signalled a major contractual crisis affecting deliveries to European buyers such as Belgium, Italy, and Poland, underscoring the global reach of a conflict that is geographically concentrated but economically diffuse.

Emerging adjustments are already visible. Europe and Asia are competing on energy spot markets and Asian buyers appears to outbid Europe for limited cargoes. Vietnam, for instance, is exploring discussions with Russian Novatek regarding potential imports of Siberian gas, reflecting a broader search for alternatives as supply risks intensify.

Infrastructure constraints further exacerbate the situation. Saudi Arabia operates the East-West (Petroline) pipeline, a ~1,200 km corridor linking its eastern oil system, centered on Abqaiq, to the Red Sea port of Yanbu, enabling crude exports that bypass the Strait of Hormuz and reach markets via the northern Suez route. However, this infrastructure is dedicated to crude oil (and, at times, natural gas liquids) and therefore provides little to no support for natural gas supply chains. Even the Red Sea route in the south is not fully secure, as the Bab el-Mandeb Strait has become increasingly vulnerable due to the activities of the Houthi movement, arguably Iran’s most active regional ally at present following the weakening of Hamas and Hezbollah and the collapse of the Assad regime in Syria. In this context, oil retains logistical flexibility, while gas remains structurally exposed.

Fragility in the Far East

Whatever the rising costs, the most acute vulnerability does not lie with major economies such as Japan, China, or South Korea, all of which possess substantial financial and fiscal capacity. Instead, the greatest risk is concentrated among fiscally and financially constrained South Asian states such as Pakistan and Bangladesh, which combine dependence on Middle Eastern energy imports (especially Qatari LNG) with limited economic resilience.

Historical precedent provides a clear warning. Following the Russian invasion of Ukraine in 2022, global energy markets experienced a shock of comparable magnitude. While the European Union managed to subsidize domestic households, countries such as Pakistan and Sri Lanka lacked both the fiscal capacity and the financial strength to raise funds on international capital markets in order to shield their populations. The consequences were severe: Sri Lanka defaulted, while Pakistan faced a balance-of-payments crisis and turned to the International Monetary Fund, simultaneously cutting imports of other essential goods.

Europe’s relative resilience reflected structural advantages, including diversified energy sources, such as gas from Norway and nuclear energy from France, high storage capacity, investment in renewable energy, and extensive LNG terminal infrastructure. By contrast, South Asian economies remain significantly more exposed.

According to data from the Harvard Atlas of Economic Complexity, India and Pakistan imported substantial quantities of LNG from Qatar and the United Arab Emirates in 2024, accounting for 15% of all Qatari exports in the case of India and 10% in the case of Pakistan, with India alone absorbing roughly half of all LNG exports from the Emirates.

Yet energy imports represent only one dimension of vulnerability. Remittance inflows constitute another critical channel. Gulf monarchies host large South Asian populations, particularly in Qatar, where nearly half of the population is of South Asian origin. These workers send significant financial transfers home, providing an essential buffer for domestic households.

According to The Economist, remittances from Gulf countries account for approximately 5.57% of GDP in Pakistan and can reach up to 8% in Nepal. Sri Lanka is relatively less exposed at 2.9%, followed by Bangladesh at 2.78%, while India stands at 1.64%. The same analysis indicates that Pakistan may face particularly severe pressure, as nearly 90% of its energy imports originate from the Middle East, representing at least 4% of GDP, a figure exceeded only by Nepal, where such imports account for approximately 6.78% of its GDP.

Macroeconomic fundamentals further highlight regional divergence. Nepal and India benefit from relatively strong buffers, including foreign exchange reserves equivalent to 10.4 and 7.5 months of imports, respectively, and comparatively low external government debt levels, at 20.9% of GDP for Nepal and 5.5% for India. By contrast, Pakistan, Bangladesh, and Sri Lanka are significantly more exposed. Pakistan’s reserves cover approximately 2.8 months of imports, with external debt at 25% of GDP. Sri Lanka exhibits similar reserve levels but the highest external government debt in the region, at 41.8% of GDP. Bangladesh performs somewhat better, with reserves covering 3.2 months of imports and external debt at 16.4% of GDP.

Rising gas prices and pressure on remittance inflows widen current account deficits and place downward pressure on domestic currencies. Because energy imports remain denominated in U.S. dollars, a legacy of the U.S.-Saudi arrangement established in the 1970s, currency depreciation increases both import costs and external debt burdens. As sovereign risk rises, access to international capital markets becomes increasingly constrained, leaving governments with limited options: draw down foreign reserves or compress imports, potentially including essential goods.

A Moderate or Severe Outcome? Deterrence, Divergence, and the Limits of Resolution

Efforts to forecast the trajectory of the conflict increasingly converge around two scenarios, moderate and severe, yet both remain highly uncertain given the historical volatility of the Middle East. Beyond economic projections, any meaningful analysis must account for the political, ideological, and geostrategic dynamics shaping decision-making in Tehran, Washington, and Tel Aviv.

Iranian foreign policy has long rested on two pillars. Endogenously, it was guided by a doctrine of strategic patience, reflected in measured responses to external provocations. Even following the assassination of the Quds Force leader Qassem Soleimani, widely regarded as a red line, Tehran responded cautiously. Similarly, earlier confrontations with Israel reflected proportional retaliation rather than uncontrolled escalation.

This restraint, however, appears to have been misinterpreted in Washington and, to some extent, in Israel, as evidence of structural weakness. In the wake of the reported death of the Supreme Leader Ali Khamenei and the lessons drawn from the 12-day confrontation with Israel in the previous year, Iran has shifted toward a doctrine closer to deterrence through punishment. The leadership in Tehran appears to have concluded that strategic patience invited further aggression.

Iran now seeks to leverage its geostrategic position to impose costs that its adversaries may find difficult to sustain. Its proximity to Gulf monarchies hosting U.S. military bases, combined with its influence over critical energy infrastructure and control of the Strait of Hormuz, provides a powerful foundation for this strategy.

Exogenously, Iran had relied for years on proxy networks, often described as the Axis of Resistance, to maintain a buffer against direct confrontation. However, recent developments suggest that this model has also failed to deliver its primary objective.

As a result, Tehran appears increasingly willing to absorb immediate costs, including damage to its military and civilian infrastructure, in pursuit of a more credible long-term deterrent. This dynamic helps explain why Iran recently rejected the 15-point peace plan proposed by the US President Donald Trump and instead advanced its own conditions for de-escalation, centered on the consolidation of credible deterrence. As part of its counter-offer, Tehran has demanded international recognition of its sovereignty, including explicit acknowledgment of its control over the Strait of Hormuz. By contrast, the United States conditioned any agreement on Iran abandoning its nuclear ambitions, dismantling its nuclear facilities, re-opening the Hormuz and suspending its ballistic missile program. Yet relinquishing the latter two would directly undermine the very foundation of Iran’s deterrence posture. It will basically eliminate the tools it has at its disposal for punishing its adversaries to establish the deterrence. In this context, Tehran’s refusal is not surprising, even in the face of promises from Washington to lift international sanctions. Iran continues to trade immediate economic costs for longer-term strategic gains.

The longer this impasse over ceasefire conditions persists, the greater the likelihood of continued escalation. As tensions intensify and Hormuz remains constrained or intermittently blocked, the prospect of a moderate scenario recedes, while the depth of the energy crisis, especially involving LNG and particularly affecting Asian markets, becomes more severe.

At the same time, even if the United States succeeds in negotiating an exit from the confrontation on terms broadly aligned with its own strategic preferences, potentially echoing past approaches seen in contexts such as Venezuela or Iraq, this does not imply that the conflict itself will come to an end. Israel remains deeply engaged and significantly more committed to sustaining military pressure. A relevant precedent can be found in Washington’s handling of the conflict with the Houthi movement. Once the costs of engagement outweighed the perceived benefits, the United States negotiated a bilateral arrangement that effectively ended its direct involvement in Yemen. Yet the broader confrontation, particularly involving Israel, the Houthis, and Saudi Arabia, continued unabated.

Iran appears to have internalized this lesson. Accepting U.S. terms and reopening Hormuz would remove a critical geostrategic lever from Tehran’s deterrence framework without guaranteeing that Israel would cease its operations. For the moment, the United States and Israel seem to share operational coordination, particularly in the use of airspace, but not a fully aligned military or political strategy. The definition of victory in Iran differs significantly between Trump and Netanyahu. For Trump, the normalization of energy markets appears to take precedence over regime change in Tehran, whereas for Israel, the latter may represent the central objective. This divergence has already been visible in the relatively cold shoulder response from the White House to Israeli strikes on Iranian gas infrastructure.

Even if regime change were to emerge as a shared objective, disagreements would likely persist regarding its implementation. Israel may favour the installation of a leadership openly aligned with its interests, potentially embodied by figures such as Reza Pahlavi, the son of the last Shah. By contrast, Washington may prefer a transition driven from within the existing system, reflecting a more pragmatic and potentially more stable alternative. The greater the divergence between U.S. and Israeli objectives and operational approaches, the lower the probability that any U.S.-led peace proposal will be accepted by Iran. In turn, this increases the likelihood of a prolonged conflict, a sustained disruption of Hormuz, and a continued drift away from a moderate scenario.

Finally, even if a ceasefire were reached and the Strait of Hormuz reopened with the approval of both the United States and Israel alongside Iran, this would not imply an immediate return to normal energy flows. Damage to Qatari gas infrastructure would require time to repair, delaying the full restoration of supply to pre-conflict capacity.

Nevertheless, the most severe scenario would involve the mining of Hormuz by Iran in response to further escalation, particularly if Israeli actions intensify and the United States aligns more closely with them. Historical experience from conflicts in Vietnam and Laos suggests that demining operations can take years before maritime routes are fully secure. Even after clearance efforts begin, residual risks would likely persist, driving up insurance costs and increasing the operational price of transit through a strait perceived as structurally unsafe. Moderate and reconciliatory turns severe and prolonged.

Bibliography:

Which country is the biggest loser from the energy shock?

Iran War's Impact on Gas Markets in Europe, Asia Will Last for Years

Iran War: U.S. and Israel at Odds Over Regime Change

Iran War: Tehran Rejects Trump's 15-Point Peace Plan, Issues Counterproposal

Europe loses its grip as LNG cargoes chase higher prices in Asia